I first spoke to Murray in 1989 when he worked with Promise Land Technologies – an AI company that improved trading signals and I worked at Futures Truth. He went from there to form his own companies and become an editor of Futures Magazine. He developed one of the best back testing platforms available today – TraderStudio. His dream was to compete with TradeStation and in his last days he saw a beta version of his software – 64 bit – and real time that could run his concepts of a trading session and a trading plan. The session was simply a singular algorithm whereas the plan was an overlay that could manage multiple sessions and utilize complex money management schemes. All this while collecting real time minute data. So congratulations my friend – you damn well did it!

I-Master

Murray co-developed this phenomena that caught the attention of almost all Futures Brokers in the late 90s and early 00s. When this system waded into the market you could see the wave it created. It became over traded but boy did it have a run.

Intermarket Convergence/Divergence

This concept did not catch on until Murray started focusing on it. He turned it into an art form and most of his focus was spent on uncovering the relationships between different markets and different derivatives. I can say that he become the leading expert in this field.

Futures Magazine

If you can get your hands on his collection of articles, I would definitely advise doing so. He touched on so many topics and explained them thoroughly. Futures was fortunate to have him onboard.

Family

He was always talking about his family and how much he cared for them. Murray was a workaholic – no doubt, but he was always there whenever they needed him.

Friends

I can’t list them all. He knew everybody. All the legends and all of them recognized him for his intelligence and innate market sense.

Legacy

Murray will be missed for being a good man – in every possible way. That is truly the best compliment I can pay his memory. His ideas will live on for sure, but we will all miss out on the great ideas he was yet to dream up.

Methods are wonderful tools that are just like functions, but you can put them right into your Analysis Technique and they can share the variables that are defined outside the Method. Here is an example that I have posted previously. Note: This was in response to a question I got on Jeff Swanson’s EasyLanguage Mastery Facebook Group.

{'(' Expected line 10, column 12 } //the t in tradeProfit. // var: double tradeProfit;

vars: mp(0); array: weekArray[5](0);

method void dayOfWeekAnalysis() {method definition} var: double tradeProfit; begin If mp = 1 and mp[1] = -1 then tradeProfit = (entryPrice(1) - entryPrice(0))*bigPointValue; If mp = -1 and mp[1] = 1 then tradeProfit = (entryPrice(0) - entryPrice(1))*bigPointValue; weekArray[dayOfWeek(entryDate(1))] = weekArray[dayOfWeek(entryDate(1))] + tradeProfit; end;

Buy next bar at highest(high,9)[1] stop; Sellshort next bar at lowest(low,9)[1] stop;

mp = marketPosition; if mp <> mp[1] then dayOfWeekAnalysis(); If lastBarOnChart then Begin print("Monday ",weekArray[1]); print("Tuesday ",weekArray[2]); print("Wednesday ",weekArray[3]); print("Thursday ",weekArray[4]); print("Friday ",weekArray[5]); end;

PowerEditor Cannot Handle Method Syntax

Convert Method to External Function

Sounds easy enough – just remove Method and copy code and put into a new function. This method keeps track of Day Of Week Analysis. So what is the function going to return? It needs to return the performance metrics for Monday, Tuesday, Wednesday, Thursday and Friday. That is five values so you can’t simply assign the Function Name a single value – right?

tradeProfit = -999999999; If mp = 1 and mp[1] = -1 then tradeProfit = (entryPrice(1) - entryPrice(0))*bigPointValue; If mp = -1 and mp[1] = 1 then tradeProfit = (entryPrice(0) - entryPrice(1))*bigPointValue; if tradeProfit <> -999999999 then weekArray[dayOfWeek(entryDate(1))] = weekArray[dayOfWeek(entryDate(1))] + tradeProfit; print(d," ",mp," ",mp[1]," ",dayOfWeek(entryDate(1)),tradeProfit," ",entryDate," ",entryDate(1)," ",entryPrice(0)," ",entryPrice(1));

DayOfWeekAnalysis = 1;

Simple Function - What's the Big Deal

Looks pretty simple and straight forward. Take a look at the first line of code. Notice how I inform the function to expect an array of [n] length to passed to it. Also notice I am not passing by value but by reference. Value versus reference – huge difference. Value is a scalar value such as 5, True or a string. When you pass by reference you are actually passing a pointer to actual location in computer memory – once you change it – it stays changed and that is what we want to do. When you pass a variable to an indicator function you are simple passing a value that is not modified within the body of the function. If you want a function to modify and return more than one value you can pass the variable and catch it as a numericRef. TradeStation has a great explanation of multiple output functions.

Multiple Output Function per EasyLanguage

Some built-in functions need to return more than a single value and do this by using one or more output parameters within the parameter list. Built-in multiple output functions typically preface the parameter name with an ‘o’ to indicate that it is an output parameter used to return a value. These are also known as ‘input-output’ parameters because they are declared within a function as a ‘ref’ type of input (i.e. NumericRef, TrueFalseRef, etc.) which allows it output a value, by reference, to a variable in the EasyLanguage code calling the function.

I personally don’t follow the “O” prefacing, but if it helps you program then go for it.

Series Function – What Is It And Why Do I Need to Worry About It?

A series function is a specialized function that refers to a previous function value within its calculations. In addition, series functions update their value on every bar even if the function call is placed within a conditional structure that may not be true on a given bar. Because a series function automatically stores its own previous values and executes on every bar, it allows you to write function calculations that may be more streamlined than if you had to manage all of the resources yourself. However, it’s a good idea to understand how this might affect the performance of your EasyLanguage code.

Seems complicated, but it really isn’t. It all boils down to SCOPE – not the mouthwash. See when you call a function all the variables inside that function are local to that particular function – in other words it doesn’t have a memory. If it changes a value in the first call to the function, it has amnesia so the next time you call the function it forgets what it did just prior – unless its a series function. Then it remembers. This is why I can do this:

If mp = 1 and mp[1] = -1 then tradeProfit = (entryPrice(1) - entryPrice(0))*bigPointValue; If mp = -1 and mp[1] = 1 then tradeProfit = (entryPrice(0) - entryPrice(1))*bigPointValue;

I Can Refer to Prior Values - It Has A Memory

Did you notice TradeProfit = -99999999 and then if it changes then I accumulate it in the correct Day Bin. If I didn’t check for this then the values in the Day Bin would be accumulated with the values returned by EntryPrice and ExitPrice functions. Remember this function is called on every bar even if you don’t call it. I could have tested if a trade occurred and passed this information to the function and then have the function access the EntryPrice and ExitPrice values. This is up to your individual taste of style. One more parameter for readability, or one less parameter for perhaps efficiency?

This Is A Special Function – Array Manipulator and Series Type

When you program a function like this the EasyLanguage Dev. Environment can determine what type of function you are using. But if you need to change it you can. Simply right click inside the editor and select Properites.

Function Properties – AutoDetect Selected

How Do You Call Such a “Special” Function?

The first thing you need to do is declare the array that you will be passing to the function. Use the keyword Array and put the number of elements it will hold and then declare the values of each element. Here I create a 5 element array and assign each element zero. Here is the function wrapper.

Buy next bar at highest(high,9)[1] stop; Sellshort next bar at lowest(low,9)[1] stop; mp = marketPosition; newTrade = False; //if mp <> mp[1] then newTrade = true;

value1 = dayOfWeekAnalysis(weekArray); If lastBarOnChart then Begin print("Monday ",weekArray[1]); print("Tuesday ",weekArray[2]); print("Wednesday ",weekArray[3]); print("Thursday ",weekArray[4]); print("Friday ",weekArray[5]); end;

Wrapper Function - Notice I only Pass the Array to the Function

Okay that’s how you convert a Method from EasyLanguage into a Function. Functions are more re-uasable, but methods are easier. But if you can’t use a method you now know how to convert one that uses Array Manipulation and us a “Series” type.

Videos Published Explaining Code for the ES.D DayTrade (V-ORBO) Strategy

Two videos have been uploaded to youTube describing the strategy and strategy based indicator that I discussed in the prior post. Here is todays action (Friday 9th of April).

2021-04-09 Friday Action – Sometimes It Works

What’s In The Videos?

Getting the Shading of the Break Out Box requires some tweaking of the indicator properties. Part A shows how to do this – remember the code is available in the prior post. In Part B I break down the code and show I first was inspired to develop the indicator and then figured developing the strategy would help create the indicator. I describe both sources in the Part B.

I didn’t say a very good Free System! This code is really cool so I thought I would share with you. Take a look at this rather cool picture.

Six Bar Break Out with Volatility Buffer and Volatility Trailing Stop

Thanks to a reader of this blog (AG), I got this idea and programmed a very simple day trading system that incorporated a volatility trailing stop. I wanted to make sure that I had it programmed correctly and always wanted to draw a box on the chart – thanks to (TJ) from MC forums for getting me going on the graphic aspect of the project.

Since I have run out of time for today – need to get a haircut. I will have to wait till tomorrow to explain the code. But real quickly the system.

Buy x% above first y bar high and then set up a trailing stop z% of y bar average range – move to break-even when profits exceed $w. Opposite goes for the short side. One long and one short only allowed during the day and exit all at the close.

if barCount >= startTradeBars then begin volAmt = average(range,startTradeBars); if barCount = startTradeBars then begin longStop = highToday + breakOutVolPer * volAmt; shortStop = lowToday - breakOutVolPer * volAmt; end; if t < endTradeTime then begin if longsToday = 0 then buy("volOrboL") next bar at longStop stop; if shortsToday = 0 then sellShort("volOrboS") next bar shortStop stop; end;

trailVolAmt = volAmt * trailVolPer; if mp = 1 then begin longsToday +=1; if c > entryPrice + breakEven$/bigPointValue then longTrail = maxList(entryPrice,longTrail); longTrail = maxList(c - trailVolAmt,longTrail); sell("L-TrlX") next bar at longTrail stop; end; if mp = -1 then begin shortsToday +=1; if c < entryPrice - breakEven$/bigPointValue then shortTrail = minList(entryPrice,shortTrail); shortTrail = minList(c + trailVolAmt,shortTrail); buyToCover("S-TrlX") next bar at shortTrail stop; end; end; setExitOnClose;

if barCount >= startTradeBars then begin volAmt = average(range,startTradeBars); if barCount = startTradeBars then begin longStop = highToday + breakOutVolPer * volAmt; shortStop = lowToday - breakOutVolPer * volAmt; for iCnt = 0 to startTradeBars-1 begin plot1[iCnt](longStop,"BuyBO",default,default,default); plot2[iCnt](shortStop,"ShrtBo",default,default,default); end;

end; if t < endTradeTime then begin if longsToday = 0 and h >= longStop then begin mp = 1; mEntryPrice = maxList(o,longStop); longsToday += 1; end; if shortsToday = 0 and l <= shortStop then begin mp = -1; mEntryPrice = minList(o,shortStop); shortsToday +=1; end; plot3(longStop,"BuyBOXTND",default,default,default); plot4(shortStop,"ShrtBOXTND",default,default,default); end;

trailVolAmt = volAmt * trailVolPer;

if mp = 1 then begin if c > mEntryPrice + breakEven$/bigPointValue then longTrail = maxList(mEntryPrice,longTrail);

longTrail = maxList(c - trailVolAmt,longTrail); plot5(longTrail,"LongTrail",default,default,default); end; if mp = -1 then begin if c < mEntryPrice - breakEven$/bigPointValue then shortTrail = minList(mEntryPrice,shortTrail); shortTrail = minList(c + trailVolAmt,shortTrail); plot6(shortTrail,"ShortTrail",default,default,default); end; end;

Cool code for the indicator

Very Important To Set Indicator Defaults Like This

For the BO Box use these settings – its the first 4 plots:

Use these colors and bar high and bar low and set opacity

The box is created by drawing thick semi-transparent lines from the BuyBo and BuyBOXTND down to ShrtBo and ShrtBOXTND. So the Buy components of the 4 first plots should be Bar High and the Shrt components should be Bar Low. I didn’t specify this the first time I posted. Thanks to one of my readers for point this out!

Use bar low for ShrtBo and ShrtBOXTND plots

Also I used different colors for the BuyBo/ShrtBo and the BuyBOXTND/ShrtBOXTND. Here is that setting:

The darker colored line on the last bar of the break out is caused by the overlap of the two sets of plots.

Here is how you set up the trailing stop plots:

Make Dots and Make Then Large – I have Red and Blue Set

Since this is part 1 we are just going to go over a very simple system: SAR (stop and reverse) at highest/lowest high/low for past 20 days.

A 2D Array in EasyLanguage is Immutable

Meaning that once you create an array all of the data types must be the same. In a Python list you can have integers, strings, objects whatever. In C and its derivatives you also have a a data structure (a thing that stores related data) know as a Structure or Struct. We can mimic a structure in EL by using a 2 dimensional array. An array is just a list of values that can be referenced by an index.

array[1] = 3.14

array[2] = 42

array[3] = 2.71828

A 2 day array is similar but it looks like a table

array[1,1], array[1,2], array[1,3]

array[2,1], array[2,2], array[2,3]

The first number in the pair is the row and the second is the column. So a 2D array can be very large table with many rows and columns. The column can also be referred to as a field in the table. To help use a table you can actually give your fields names. Here is a table structure that I created to store trade information.

trdEntryPrice (0) – column zero – yes we can have a 0 col. and row

trdEntryDate(1)

trdExitPrice (2)

trdExitDate(3)

trdID(4)

trdPos(5)

trdProfit(6)

trdCumuProfit(7)

So when I refer to tradeStruct[0, trdEntryPrice] I am referring to the first column in the first row.

This how you define a 2D array and its associate fields.

In EasyLanguage You are Poised at the Close of a Yesterday’s Bar

This paradigm allows you to sneak a peek at tomorrow’s open tick but that is it. You can’t really cheat, but it also limits your creativity and makes things more difficult to program when all you want is an accurate backtest. I will go into detail, if I haven’t already in an earlier post, the difference of sitting on Yesterday’s close verus sitting on Today’s close with retroactive trading powers. Since we are only storing trade information when can use hindsight to gather the information we need.

Buy tomorrow at highest(h,20) stop;

SellShort tomorrow at lowest(l,20) stop;

These are the order directives that we will be using to execute our strategy. We can also run a Shadow System, with the benefit of hindsight, to see where we entered long/short and at what prices. I call it a Shadow because its all the trades reflected back one bar. All we need to do is offset the highest and lowest calculations by 1 and compare the values to today’s highs and lows to determine trade entry. We must also test the open if a gap occurred and we would have been filled at the open. Now this code gets a bit hairy, but stick with it.

if mPos <> 1 then begin if h >= stb1 then begin if mPos < 0 then // close existing short position begin mEntryPrice = tradeStruct[numTrades,trdEntryPrice]; mExitPrice = maxList(o,stb1); tradeStruct[numTrades,trdExitPrice] = mExitPrice; tradeStruct[numTrades,trdExitDate] = date; mProfit = (mEntryPrice - mExitPrice) * bigPointValue - mCommSlipp; cumuProfit += mProfit; tradeStruct[numTrades,trdCumuProfit] = cumuProfit; tradeStruct[numTrades,trdProfit] = mProfit; print(d+19000000:8:0," shrtExit ",mEntryPrice:4:5," ",mExitPrice:4:5," ",mProfit:6:0," ",cumuProfit:7:0); print("-------------------------------------------------------------------------"); end; numTrades +=1; mEntryPrice = maxList(o,stb1); tradeStruct[numTrades,trdID] = 1; tradeStruct[numTrades,trdPOS] = 1; tradeStruct[numTrades,trdEntryPrice] = mEntryPrice; tradeStruct[numTrades,trdEntryDate] = date; mPos = 1; print(d+19000000:8:0," longEntry ",mEntryPrice:4:5); end; end; if mPos <>-1 then begin if l <= sts1 then begin if mPos > 0 then // close existing long position begin mEntryPrice = tradeStruct[numTrades,trdEntryPrice]; mExitPrice = minList(o,sts1); tradeStruct[numTrades,trdExitPrice] = mExitPrice; tradeStruct[numTrades,trdExitDate] = date; mProfit = (mExitPrice - mEntryPrice ) * bigPointValue - mCommSlipp; cumuProfit += mProfit; tradeStruct[numTrades,trdCumuProfit] = cumuProfit; tradeStruct[numTrades,trdProfit] = mProfit; print(d+19000000:8:0," longExit ",mEntryPrice:4:5," ",mExitPrice:4:5," ",mProfit:6:0," ",cumuProfit:7:0); print("---------------------------------------------------------------------"); end; numTrades +=1; mEntryPrice =minList(o,sts1); tradeStruct[numTrades,trdID] = 2; tradeStruct[numTrades,trdPOS] =-1; tradeStruct[numTrades,trdEntryPrice] = mEntryPrice; tradeStruct[numTrades,trdEntryDate] = date; mPos = -1; print(d+19000000:8:0," ShortEntry ",mEntryPrice:4:5); end; end;

Shadow System - Generic forany SAR System

Notice I have stb and stb1. The only difference between the two calculations is one is displaced a day. I use the stb and sts in the EL trade directives. I use stb1 and sts1 in the Shadow System code. I guarantee this snippet of code is in every backtesting platform out there.

All the variables that start with the letter m, such as mEntryPrice, mExitPrice deal with the Shadow System. Theyare not derived from TradeStation’s back testing engine only our logic. Lets look at the first part of just one side of the Shadow System:

if mPos <> 1 then begin if h >= stb1 then begin if mPos < 0 then // close existing short position begin mEntryPrice = tradeStruct[numTrades,trdEntryPrice]; mExitPrice = maxList(o,stb1); tradeStruct[numTrades,trdExitPrice] = mExitPrice; tradeStruct[numTrades,trdExitDate] = date; mProfit = (mEntryPrice - mExitPrice) * bigPointValue - mCommSlipp; cumuProfit += mProfit; tradeStruct[numTrades,trdCumuProfit] = cumuProfit; tradeStruct[numTrades,trdProfit] = mProfit; print(d+19000000:8:0," shrtExit ",mEntryPrice:4:5," ",mExitPrice:4:5," ",mProfit:6:0," ",cumuProfit:7:0); print("-------------------------------------------------------------------------"); end;

mPos and mEntryPrice and mExitPrice belong to the Shadow System

if mPos <> 1 then the Shadow Systems [SS] is not long. So we test today’s high against stb1 and if its greater then we know a long position was put on. But what if mPos = -1 [short], then we need to calculate the exit and the trade profit and the cumulative trade profit. If mPos = -1 then we know a short position is on and we can access its particulars from the tradeStruct 2D array. mEntryPrice = tradeStruct[numTrades,trdEntryPrice]. We can gather the other necessary information from the tradeStruct [remember this is just a table with fields spelled out for us.] Once we get the information we need we then need to stuff our calculations back into the Structure or table so we can regurgitate later. We stuff date in to the following fields trdExitPrice, trdExitDate, trdProfit and trdCumuProfit in the table.

Formatted Print: mEntryPrice:4:5

Notice in the code how I follow the print out of variables with :8:0 or :4:5? I am telling TradeStation to use either 0 or 5 decimal places. The date doesn’t need decimals but prices do. So I format that so that they will line up really pretty like.

Now that I take care of liquidating an existing position all I need to do is increment the number of trades and stuff the new trade information into the Structure.

The same goes for the short entry and long exit side of things. Just review the code. I print out the trades as we go along through the history of crude. All the while stuffing the table.

If LastBarOnChart -> Regurgitate

On the last bar of the chart we know exactly how many trades have been executed because we were keeping track of them in the Shadow System. So it is very easy to loop from 0 to numTrades.

if lastBarOnChart then begin print("Trade History"); for arrIndx = 1 to numTrades begin value20 = tradeStruct[arrIndx,trdEntryDate]; value21 = tradeStruct[arrIndx,trdEntryPrice]; value22 = tradeStruct[arrIndx,trdExitDate]; value23 = tradeStruct[arrIndx,trdExitPrice]; value24 = tradeStruct[arrIndx,trdID]; value25 = tradeStruct[arrIndx,trdProfit]; value26 = tradeStruct[arrIndx,trdCumuProfit];

print("---------------------------------------------------------------------"); if value24 = 1 then begin string1 = buyStr; string2 = sellStr; end; if value24 = 2 then begin string1 = shortStr; string2 = coverStr; end; print(value20+19000000:8:0,string1,value21:4:5," ",value22+19000000:8:0,string2, value23:4:5," ",value25:6:0," ",value26:7:0); end; end;

Add 19000000 to Dates for easy Translation

Since all trade information is stored in the Structure or Table then pulling the information out using our Field Descriptors is very easy. Notice I used EL built-in valueXX to store table information. I did this to make the print statements a lot shorter. I could have just used tradeStruct[arrIndx, trdEntry] or whatever was needed to provide the right information, but the lines would be hard to read. To translate EL date to a normal looking data just add 19,000,000 [without commas].

If you format your PrintLog to a monospaced font your out put should look like this.

PrintLog OutPut

Why Would We Want to Save Trade Information?

The answer to this question will be answered in Part 2. Email me with any other questions…..

Why Can’t I Just Test with Daily Bars and Use Look-Inside Bar?

Good question. You can’t because it doesn’t work accurately all of the time. I just default to using 5 minute or less bars whenever I need to. A large portion of short term, including day trade, systems need to know the intra day market movements to know which orders were filled accurately. It would be great if you could just flip a switch and convert a daily bar system to an intraday system and Look Inside Bar(LIB) is theoretically that switch. Here I will prove that switch doesn’t always work.

Daily Bar System

Buy next bar at open of the day plus 20% of the 5 day average range

SellShort next at open of the day minus 20% of the 5 day average range

If long take a profit at one 5 day average range above entryPrice

If short take a profit at one 5 day average range below entryPrice

If long get out at a loss at 1/2 a 5 day average range below entryPrice

If short get out at a loss at 1/2 a 5 day average range above entry price

Simplified Daily Bar DayTrade System using ES.D Daily

Daily Bar Using 5 min Look Inside Bar

Looks great with just the one hiccup: Bot @ 3846.75 and the Shorted @ 3834.75 and then took nearly 30 handles of profit.

Now let’s see what really happened.

What Really Happened – Bot – Shorted – Stopped Out

Intraday Code to Control Entry Time and Number of Longs and Shorts

Not an accurate representation so let’s take this really simple system and apply it to intraday data. Approaching this from a logical perspective with limited knowledge about TradeStation you might come up with this seemingly valid solution. Working on the long side first.

//First Attempt

if d <> d[1] then value1 = .2 * average(Range of data2,5); value2 = value1 * 5; if t > sess1startTime then buy next bar at opend(0) + value1 stop; setProfitTarget(value2*bigPointValue); setStopLoss(value2/2*bigPointValue); setExitOnClose;

First Simple Attempt

This looks very similar to the daily bar system. I cheated a little by using

if d <> d[1] then value1 = .2 * average(Range of data2,5);

Here I am only calculating the average once a day instead of on each 5 minute bar. Makes things quicker. Also I used

if t > sess1StartTime then buy next bar at openD(0) + value1 stop;

I did that because if you did this:

buy next bar at open of next bar + value1 stop;

You would get this:

Cannot Sneak a Peek with Data2

That should do it for the long side, right?

Didn’t work quite right!

So now we have to monitor when we can place a trade and monitor the number of long and short entries.

How does this look!

Correct Execution!

So here is the code. You will notice the added complexity. The important things to know is how to control when an entry is allowed and how to count the number of long and short entries. I use the built-in keyword/function totalTrades to keep track of entries/exits and marketPosition to keep track of the type of entry.

Take a look at the code and you can see how the daily bar system is somewhat embedded in the code. But remember you have to take into account that you are stepping through every 5 minute bar and things change from one bar to the next.

if d <> d[1] then begin curTotTrades = totalTrades; value1 = .2 * average(Range of data2,5); value2 = value1 * 5; buysToday = 0; shortsToday = 0; tradeZoneTime = False; end;

mp = marketPosition;

if totalTrades > curTotTrades then begin if mp <> mp[1] then begin if mp[1] = 1 then buysToday = buysToday + 1; if mp[1] = -1 then shortsToday = shortsToday + 1; end; if mp[1] = -1 then print(d," ",t," ",mp," ",mp[1]," ",shortsToday); curTotTrades = totalTrades; end; if t > sess1StartTime and t < sess1EndTime then tradeZoneTime = True;

if tradeZoneTime and buysToday = 0 and mp <> 1 then buy next bar at opend(0) + value1 stop;

if tradeZoneTime and shortsToday = 0 and mp <> -1 then sellShort next bar at opend(0) - value1 stop;

Proper Code to Replicate the Daily Bar System with Accuracy

Here’s a few trade examples to prove our code works.

Looks Right!

Okay the code worked but did the system?

Uh? NO!

Conclusion

If you need to know what occurred first – a high or a low in a move then you must use intraday data. If you want to have multiple entries then of course your only alternative is intraday data. This little bit of code can get you started converting your daily bar systems to intraday data and can be a framework to develop your own day trading/or swing systems.

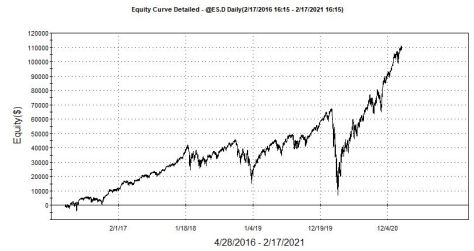

Can I Prototype A Short Term System with Daily Data?

You can of course use Daily Bars for fast system prototyping. When the daily bar system was tested with LIB turned on, it came close to the same results as the more accurately programmed intraday system. So you can prototype to determine if a system has a chance. Our core concept buyt a break out, short a break out, take profits and losses and have no overnight exposure sounds good theoretically. And if you only allow 2 entries in opposite directions on a daily bar you can determine if there is something there.

A Dr. Jekyll and Mr. Hyde Scenario

While playing around with this I did some prototyping of a daily bar system and created this equity curve. I mistakenly did not allow any losses – only took profits and re-entered long.

In this post I simply wanted to convert the intraday ratcheting stop mechanism that I previously posted into a daily bar mechanism. Well that got me thinking of how many different values could be used as the amount to ratchet. I came up with three:

I have had requests for the EasyLanguage in an ELD – so here it is – just click on the link and unZip.

So this was going to be a great start to a post, because I was going to incorporate one of my favorite programming constructs : Switch-Case. After doing the program I thought wouldn’t it be really cool to be able to optimize over each scheme the ratchet and trail multiplier as well as the values that might go into each scheme.

In scheme one I wanted to optimize the N days for the ATR calculation. In scheme two I wanted to optimize the $ amount and the scheme three the percentage of a 20 day standard deviation. I could do a stepwise optimization and run three independent optimizations – one for each scheme. Why not just do one global optimization you might ask? You could but it would be a waste of computer time and then you would have to sift through the results. Huh? Why? Here is a typical optimization loop:

Scheme

Ratchet Mult

Trigger Mult

Parameter 1

1 : ATR

1

1

ATR (2)

2 : $ Amt

1

1

ATR (2)

3 : % of Dev. Amt

1

1

ATR (2)

1 : ATR

2

1

ATR (2)

2 : $ Amt

2

1

ATR (2)

Notice when we switch schemes the Parameter 1 doesn’t make sense. When we switch to $ Amt we want to use a $ Value as Parameter 1 and not ATR. So we could do a bunch of optimizations across non sensical values, but that wouldn’t really make a lot of sense. Why not do a conditional optimization? In other words, optimize only across a certain parameter range based on which scheme is currently being used. I knew there wasn’t an overlay available to use using standard EasyLanguage but I thought maybe OOP, and there is an optimization API that is quite powerful. The only problem is that it was very complicated and I don’t know if I could get it to work exactly the way I wanted.

EasyLanguage is almost a full blown programming language. So should I not be able to distill this conditional optimization down to something that I could do with such a powerful programming language? And the answer is yes and its not that complicated. Well at least for me it wasn’t but for beginners probably. But to become a successful programmer you have to step outside your comfort zones, so I am going to not only explain the Switch/Case construct (I have done this in earlier posts) but incorporate some array stuff.

When performing conditional optimization there are really just a few things you have to predefine:

Scheme Based Optimization Parameters

Exact Same Number of Iterations for each Scheme [starting point and increment value]

Complete Search Space

Total Number of Iterations

Staying inside the bounds of your Search Space

Here are the optimization range per scheme:

Scheme #1 – optimize number of days in ATR calculation – starting at 10 days and incrementing by 2 days

Scheme #2 – optimize $ amounts – starting at $250 and incrementing by $100

Scheme #3 – optimize percent of 20 Bar standard deviation – starting at 0,25 and incrementing by 0.25

I also wanted to optimize the ratchet and target multiplier. Here is the base code for the daily bar ratcheting system with three different schemes. Entries are based on penetration of 20 bar highest/lowest close.

if volBase then begin ratchetAmt = avgTrueRange(volCalcLen) * ratchetMult; trailAmt = avgTrueRange(volCalcLen) * trailMult; end; if dollarBase then begin ratchetAmt =dollarAmt/bigPointValue * ratchetMult; trailAmt = dollarAmt/bigPointValue * trailMult; end; if devBase then begin ratchetAmt = stddev(c,20) * devAmt * ratchetMult; trailAmt = stddev(c,20) * devAmt * trailMult; end;

if c crosses over highest(c[1],20) then buy next bar at open; if c crosses under lowest(c[1],20) then sellshort next bar at open;

mp = marketPosition; if mp <> 0 and mp[1] <> mp then begin longMult = 0; shortMult = 0; end;

If mp = 1 then lep = entryPrice; If mp =-1 then sep = entryPrice;

// Okay initially you want a X point stop and then pull the stop up // or down once price exceeds a multiple of Y points // longMult keeps track of the number of Y point multiples of profit // always key off of lep(LONG ENTRY POINT) // notice how I used + 1 to determine profit // and - 1 to determine stop level

If mp = 1 then Begin If h >= lep + (longMult + 1) * ratchetAmt then longMult = longMult + 1; Sell("LongTrail") next bar at (lep + (longMult - 1) * trailAmt) stop; end;

If mp = -1 then Begin If l <= sep - (shortMult + 1) * ratchetAmt then shortMult = shortMult + 1; buyToCover("ShortTrail") next bar (sep - (shortMult - 1) * trailAmt) stop; end;

Daily Bar Ratchet System

This code is fairly simple. The intriguing inputs are:

volBase[True of False] and volCalcLen [numeric Value]

dollarBase [True of False] and dollarAmt [numeric Value]

devBase [True of False] and devAmt [numeric Value]

If volBase is true then you use the parameters that go along with that scheme. The same goes for the other schemes. So when you run this you would turn one scheme on at a time and set the parameters accordingly. if I wanted to use dollarBase(True) then I would set the dollarAmt to a $ value. The ratcheting mechanism is the same as it was in the prior post so I refer you back to that one for further explanation.

So this was a pretty straightforward strategy. Let us plan out our optimization search space based on the different ranges for each scheme. Since each scheme uses a different calculation we can’t simply optimize across all of the different ranges – one is days, and the other two are dollars and percentages.

Enumerate

We know how to make TradeStation loop based on the range of a value. If you want to optimize from $250 to $1000 in steps of $250, you know this involves [$1000 – $250] / $250 + 1 or 3 + 1 or 4 interations. Four loops will cover this entire search space. Let’s examine the search space for each scheme:

ATR Scheme: start at 10 bars and end at 40 by steps of 2 or [40-10]/2 + 1 = 16

$ Amount Scheme: start at $250 and since we have to have 16 iterations [remember # of iterations have to be the same for each scheme] what can we do to use this information? Well if we start $250 and step by $100 we cover the search space $250, $350, $450, $550…$1,750. $250 + 15 x 250. 15 because $250 is iteration 1.

Percentage StdDev Scheme: start at 0.25 and end at 0.25 + 15 x 0.25 = 4

So we enumerate 16 iterations to a different value. The easiest way to do this is to create a map. I know this seems to be getting hairy but it really isn’t. The map will be defined as an array with 16 elements. The array will be filled with the search space based on which scheme is currently being tested. Take a look at this code where I show how to define an array of 16 elements and introduce my Switch/Case construct.

array: optVals[16](0);

switch(switchMode) begin case 1: startPoint = 10; // vol based increment = 2; case 2: startPoint = 250/bigPointValue; // $ based increment = 100/bigPointValue; case 3: startPoint = 0.25; //standard dev increment = 0.25*minMove/priceScale; default: startPoint = 1; increment = 1; end;

vars: cnt(0),loopCnt(0); once begin for cnt = 1 to 16 begin optVals[cnt] = startPoint + (cnt-1) * increment; end; end

Set Up Complete Search Space for all Three Schemes

This code creates a 16 element array, optVals, and assigns 0 to each element. SwitchMode goes from 1 to 3.

if switchMode is 1: ATR scheme [case: 1] the startPoint is set to 10 and increment is set to 2

if switchMode is 2: $ Amt scheme [case: 2] the startPoint is set to $250 and increment is set to $100

if switchMode is 3: Percentage of StdDev [case: 3] the startPoint is set to 0.25 and the increment is set to 0.25

Once these two values are set the following 15 values can be spawned by the these two. A for loop is great for populating our search space. Notice I wrap this code with ONCE – remember ONCE is only executed at the very beginning of each iteration or run.

once begin for cnt = 1 to 16 begin optVals[cnt] = startPoint + (cnt-1) * increment; end; end

Based on startPoint and increment the entire search space is filled out. Now all you have to do is extract this information stored in the array based on the iteration number.

if c crosses over highest(c[1],20) then buy next bar at open; if c crosses under lowest(c[1],20) then sellshort next bar at open;

mp = marketPosition; if mp <> 0 and mp[1] <> mp then begin longMult = 0; shortMult = 0; end;

If mp = 1 then lep = entryPrice; If mp =-1 then sep = entryPrice;

// Okay initially you want a X point stop and then pull the stop up // or down once price exceeds a multiple of Y points // longMult keeps track of the number of Y point multiples of profit // always key off of lep(LONG ENTRY POINT) // notice how I used + 1 to determine profit // and - 1 to determine stop level

If mp = 1 then Begin If h >= lep + (longMult + 1) * ratchetAmt then longMult = longMult + 1; Sell("LongTrail") next bar at (lep + (longMult - 1) * trailAmt) stop; end;

If mp = -1 then Begin If l <= sep - (shortMult + 1) * ratchetAmt then shortMult = shortMult + 1; buyToCover("ShortTrail") next bar (sep - (shortMult - 1) * trailAmt) stop; end;

Extract Search Space Values and Rest of Code

Switch(switchMode) Begin Case 1: ratchetAmt = avgTrueRange(optVals[optLoops])ratchetMult; trailAmt = avgTrueRange(optVals[optLoops]) trailMult; Case 2: ratchetAmt =optVals[optLoops] * ratchetMult; trailAmt = optVals[optLoops] * trailMult; Case 3: ratchetAmt =stddev(c,20)optVals[optLoops] ratchetMult; trailAmt = stddev(c,20) * optVals[optLoops] * trailMult;

Notice how the optVals are indexed by optLoops. So the only variable that is optimized is the optLoops and it spans 1 through 16. This is the power of enumerations – each number represents a different thing and this is how you can control which variables are optimized in terms of another optimized variable. Here is my optimization specifications:

Opimization space

And here are the results:

Optimization Results

The best combination was scheme 1 [N-day ATR Calculation] using a 2 Mult Ratchet and 1 Mult Trail Trigger. The best N-day was optVals[2] for this scheme. What in the world is this value? Well you will need to back engineer a little bit here. The starting point for this scheme was 10 and the increment was 2 so if optVals[1] =10 then optVals[2] = 12 or ATR(12). You can also print out a map of the search spaces.

vars: cnt(0),loopCnt(0); once begin loopCnt = loopCnt + 1; // print(switchMode," : ",d," ",startPoint); // print(" ",loopCnt:2:0," --------------------"); for cnt = 1 to 16 begin optVals[cnt] = startPoint + (cnt-1) * increment; // print(cnt," ",optVals[cnt]," ",cnt-1); end; end;

This was a elaborate post so please email me with questions. I wanted to demonstrate that we can accomplish very sophisticated things with just the pure and raw EasyLanguage which is a programming language itself.

A reader of this blog wanted a conversion from my Ratchet Trailing Stop indicator into a Strategy. You will notice a very close similarity with the indicator code as the code for this strategy. This is a simple N-Bar [Hi/Lo] break out with inputs for the RatchetAmt and TrailAmt. Remember RatchetAmt is how far the market must move in your favor before the stop is pulldown the TrailAmt. So if the RatchetAmt is 12 and the TrailAmt is 6, the market would need to move 12 handles in your favor and the Trail Stop would move to break even. If it moves another 12 handles then the stop would be moved up/down by 6 handles. Let me know if you have any questions – this system is similar to the one I just posted.

Notice how the RED line Ratchets Up by the Fixed Amount [8/6]

If d <> d[1] then Begin longMult = 0; shortMult = 0; myBarCount = 0; mp = 0; lep = 0; sep = 0; buysToday = 0; shortsToday = 0; end;

myBarCount = myBarCount + 1;

If myBarCount = 6 then // six 5 min bars = 30 minutes Begin stb = highD(0); //get the high of the day sts = lowD(0); //get low of the day end;

If myBarCount >=6 and t < calcTime(sess1Endtime,-3*barInterval) then Begin if buysToday = 0 then buy("NBar-Range-B") next bar stb stop; if shortsToday = 0 then sellShort("NBar-Range-S") next bar sts stop; end;

mp = marketPosition; If mp = 1 then begin lep = entryPrice; buysToday = 1; end; If mp =-1 then begin sep = entryPrice; shortsToday = 1; end;

// Okay initially you want a X point stop and then pull the stop up // or down once price exceeds a multiple of Y points // longMult keeps track of the number of Y point multipes of profit // always key off of lep(LONG ENTRY POINT) // notice how I used + 1 to determine profit // and - 1 to determine stop level

If mp = 1 then Begin If h >= lep + (longMult + 1) * ratchetAmt then longMult = longMult + 1; Sell("LongTrail") next bar at (lep + (longMult - 1) * trailAmt) stop; end;

If mp = -1 then Begin If l <= sep - (shortMult + 1) * ratchetAmt then shortMult = shortMult + 1; buyToCover("ShortTrail") next bar (sep - (shortMult - 1) * trailAmt) stop; end;

setExitOnClose;

I Used my Ratchet Indicator for the Basis of this Strategy

What is Better: 30, 60, or 120 Minute Break-Out on ES.D

Here is a simple tutorial you can use as a foundation to build a potentially profitable day trading system. Here we wait N minutes after the open and then buy the high of the day or short the low of the day and apply a protective stop and profit objective. The time increment can be optimized to see what time frame is best to use. You can also optimize the stop loss and profit objective – this system gets out at the end of the day. This system can be applied to any .D data stream in TradeStation or Multicharts.

Logic Description

get open time

get close time

get N time increment

15 – first 15 minute of day

30 – first 30 minute of day

60 – first hour of day

get High and Low of day

place stop orders at high and low of day – no entries late in day

calculate buy and short entries – only allow one each*

apply stop loss

apply profit objective

get out at end of day if not exits have occurred

Optimization Results [From 15 to 120 by 5 minutes] on @ES.D 5 Minute Chart – Over Last Two Years

Optimization of Time: Look How the # Trades Decrease as the Time Increment Increases

Simple Orbo EasyLanguage

I threw this together rather quickly in a response to a reader’s question. Let me know if you see a bug or two. Remember once you gather your stops you must allow the order to be issued on every subsequent bar of the trading day. The trading day is defined to be the time between timeIncrement and endTradeMinB4Close. Notice how I used the EL function calcTime to calculate time using either a +positive or -negative input. I want to sample the high/low of the day at timeIncrement and want to trade up until endTradeMinB4Close time. I use the HighD and LowD functions to extract the high and low of the day up to that point. Since I am using a tight stop relative to today’s volatility you will see more than 1 buy or 1 short occurring. This happens when entry/exit occurs on the same bar and MP is not updated accordingly. Somewhere hidden in this tome of a blog you will see a solution for this. If you don’t want to search I will repost it tomorrow.

//Optimizing Time to determine a simple break out //Only works on .D data streams Inputs: timeIncrement(15),endTradeMinB4Close(-15),stopLoss$(500),profTarg$(1000);

If time = calcStopTime then begin buyStop = HighD(0); shortStop = LowD(0); buysToday = 0; shortsToday = 0; End;

if time >= calcStopTime and time < quitTradeTime then begin if buysToday = 0 then Buy next bar at buyStop stop; if shortsToday = 0 then Sell short next bar at shortStop stop; end;

mp = marketPosition;

If mp = 1 then buysToday = 1; If mp = -1 then shortsToday = 1;

I was recently testing the idea of a short term VBO strategy on the ES utilizing very tight stops. I wanted to see if using a tight ATR stop in concert with the entry day’s low (for buys) would cut down on losses after a break out. In other words, if the break out doesn’t go as anticipated get out and wait for the next signal. With the benefit of hindsight in writing this post, I certainly felt like my exit mechanism was what was going to make or break this system. In turns out that all pre conceived notions should be thrown out when volatility enters the picture.

System Description

If 14 ADX < 20 get ready to trade

Buy 1 ATR above the midPoint of the past 4 closing prices

Place an initial stop at 1 ATR and a Profit Objective of 1 ATR

Trail the stop up to the prior day’s low if it is greater than entryPrice – 1 ATR initially, and then trail if a higher low is established

Wait 3 bars to Re-Enter after going flat – Reversals allowed

That’s it. Basically wait for a trendless period and buy on the bulge and then get it out if it doesn’t materialize. I knew I could improve the system by optimizing the parameters but I felt I was in the ball park. My hypothesis was that the system would fail because of the tight stops. I felt the ADX trigger was OK and the BO level would get in on a short burst. Just from past experience I knew that using the prior day’s price extremes as a stop usually doesn’t fair that well.

Without commission the initial test was a loser: -$1K and -$20K draw down over the past ten years. I thought I would test my hypothesis by optimizing a majority of the parameters:

ADX Len

ADX Trigger Value

ATR Len

ATR BO multiplier

ATR Multiplier for Trade Risk

ATR Multiplier for Profit Objective

Number of bars to trail the stop – used lowest lows for longs

Results

As you can probably figure, I had to use the Genetic Optimizer to get the job done. Over a billion different permutations. In the end here is what the computer pushed out using the best set of parameters.

No Commission or Slippage – Genetic Optimized Parameter Selection

Optimization Report – The Best of the Best

Top Parameters – notice the Wide Stop Initially and the Trailing Stop Look-Back and also the Profit Multiplier – but what really sticks out is the ADX inputs

ADX – Does it Really Matter?

Take a look at the chart – the ADX is mostly in Trigger territory – does it really matter?

A Chart is Worth a 1000 Words

What does this chart tell us?

70% of Profit was made in last 40 trades

Was the parameter selection biased by the heightened level of volatility? The system has performed on the parameter set very well over the past two or three years. But should you use this parameter set going into the future – volatility will eventually settle down.

Now using my experience in trading I would have selected a different parameter set. Here are my biased results going into the initial programming. I would use a wider stop for sure, but I would have used the generic ADX values.

George’s More Common Sense Parameter Selection – wow big difference

I would have used 14 ADX Len with a 20 trigger and risk 1 to make 3 and use a wider trailing stop. With trend neutral break out algorithms, it seems you have to be in the game all of the time. The ADX was supposed to capture zones that predicated break out moves, but the ADX didn’t help out at all. Wider stops helped but it was the ADX values that really changed the complexion of the system. Also the number of bars to wait after going flat had a large impact as well. During low volatility you can be somewhat picky with trades but when volatility increases you gots to be in the game. – no ADX filtering and no delay in re-Entry. Surprise, surprise!

Alogorithm Code

Here is the code – some neat stuff here if you are just learning EL. Notice how I anchor some of the indicator based variables by indexing them by barsSinceEntry. Drop me a note if you see something wrong or want a little further explanation.

If mp <> 1 and adx(adxLen) < adxTrig and BSE > reEntryDelay and open of next bar < BBO then buy next bar at BBO stop; If mp <>-1 and adx(adxLen) < adxTrig AND BSE > reEntryDelay AND open of next bar > SBO then sellshort next bar at SBO stop;

If mp = 1 and mp[1] <> 1 then Begin trailLongStop = entryPrice - tradeRisk; end;

If mp = -1 and mp[1] <> -1 then Begin trailShortStop = entryPrice + tradeRisk; end;

if mp = 1 then sell("L-init-loss") next bar at entryPrice - tradeRisk[barsSinceEntry] stop; if mp = -1 then buyToCover("S-init-loss") next bar at entryPrice + tradeRisk[barsSinceEntry] stop;

if mp = 1 then begin sell("L-ATR-prof") next bar at entryPrice + tradeProf[barsSinceEntry] limit; trailLongStop = maxList(trailLongStop,lowest(l,posMovTrailNumBars)); sell("L-TL-Stop") next bar at trailLongStop stop; end; if mp =-1 then begin buyToCover("S-ATR-prof") next bar at entryPrice -tradeProf[barsSinceEntry] limit; trailShortStop = minList(trailShortStop,highest(h,posMovTrailNumBars)); // print(d, " Short and trailStop is : ",trailShortStop); buyToCover("S-TL-Stop") next bar at trailShortStop stop; end;

Backtesting with [Trade Station,Python,AmiBroker, Excel]. Intended for informational and educational purposes only!

Get All Five Books in the Easing Into EasyLanguage Series - The Trend Following Edition is now Available!

Announcement – A Trend Following edition has been added to my Easing into EasyLanguage Series! This edition will be the fifth and final installment and will utilize concepts discussed in the Foundation editions. I will pay respect to the legends of Trend Following by replicating the essence of their algorithms. Learn about the most prominent form of algorithmic trading. But get geared up for it by reading the first four editions in the series now. Get your favorite QUANT the books they need!

The Foundation Edition. The first in the series.

This series includes five editions that covers the full spectrum of the EasyLanguage programming language. Fully compliant with TradeStation and mostly compliant with MultiCharts. Start out with the Foundation Edition. It is designed for the new user of EasyLanguage or for those you would like to have a refresher course. There are 13 tutorials ranging from creating Strategies to PaintBars. Learn how to create your own functions or apply stops and profit objectives. Ever wanted to know how to find an inside day that is also a Narrow Range 7 (NR7?) Now you can, and the best part is you get over 4 HOURS OF VIDEO INSTRUCTION – one for each tutorial.

Hi-Res Edition Cover

This book is ideal for those who have completed the Foundation Edition or have some experience with EasyLanguage, especially if you’re ready to take your programming skills to the next level. The Hi-Res Edition is designed for programmers who want to build intraday trading systems, incorporating trade management techniques like profit targets and stop losses. This edition bridges the gap between daily and intraday bar programming, making it easier to handle challenges like tracking the sequence of high and low prices within the trading day. Plus, enjoy 5 hours of video instruction to guide you through each tutorial.

Advanced Topics Cover

The Advanced Topics Edition delves into essential programming concepts within EasyLanguage, offering a focused approach to complex topics. This book covers arrays and fixed-length buffers, including methods for element management, extraction, and sorting. Explore finite state machines using the switch-case construct, text graphic manipulation to retrieve precise X and Y coordinates, and gain insights into seasonality with the Ruggiero/Barna Universal Seasonal and Sheldon Knight Seasonal methods. Additionally, learn to build EasyLanguage projects, integrate fundamental data like Commitment of Traders, and create multi-timeframe indicators for comprehensive analysis.

Get Day Trading Edition Today!

The Day Trading Edition complements the other books in the series, diving into the popular approach of day trading, where overnight risk is avoided (though daytime risk still applies!). Programming on high-resolution data, such as five- or one-minute bars, can be challenging, and this book provides guidance without claiming to be a “Holy Grail.” It’s not for ultra-high-frequency trading but rather for those interested in techniques like volatility-based breakouts, pyramiding, scaling out, and zone-based trading. Ideal for readers of the Foundation and Hi-Res editions or those with EasyLanguage experience, this book offers insights into algorithms that shaped the day trading industry.

Trend Following Cover.

For thirty-one years as the Director of Research at Futures Truth Magazine, I had the privilege of collaborating with renowned experts in technical analysis, including Fitschen, Stuckey, Ruggiero, Fox, and Waite. I gained invaluable insights as I watched their trend-following methods reach impressive peaks, face sharp declines, and ultimately rebound. From late 2014 to early 2020, I witnessed a dramatic downturn across the trend-following industry. Iconic systems like Aberration, CatScan, Andromeda, and Super Turtle—once thriving on robust trends of the 1990s through early 2010s—began to falter long before the pandemic. Since 2020 we have seen the familiar trends return. Get six hours of video instruction with this edition.

Pick up your copies today – e-Book or paperback format – at Amazon.com